PAYE is a system that many employers use to pay tax and National Insurance for their employees. Under the PAYE system, employers calculate and deduct what you’re due to pay in tax and National Insurance from your pay cheque. They send it straight to HMRC, then they send you the rest. If you’re employed and don’t have to complete a self assessment, you likely pay your taxes through PAYE. However, just because your employer is calculating your deductions for you doesn’t mean you shouldn’t keen an eye on them, too. To help with this, HMRC will send you a variety of PAYE tax forms over the course of the year. Here, we’ll look into what each one of these PAYE tax forms is, why you get sent them, and what to look out for. Let’s get stuck in!

Your payslips

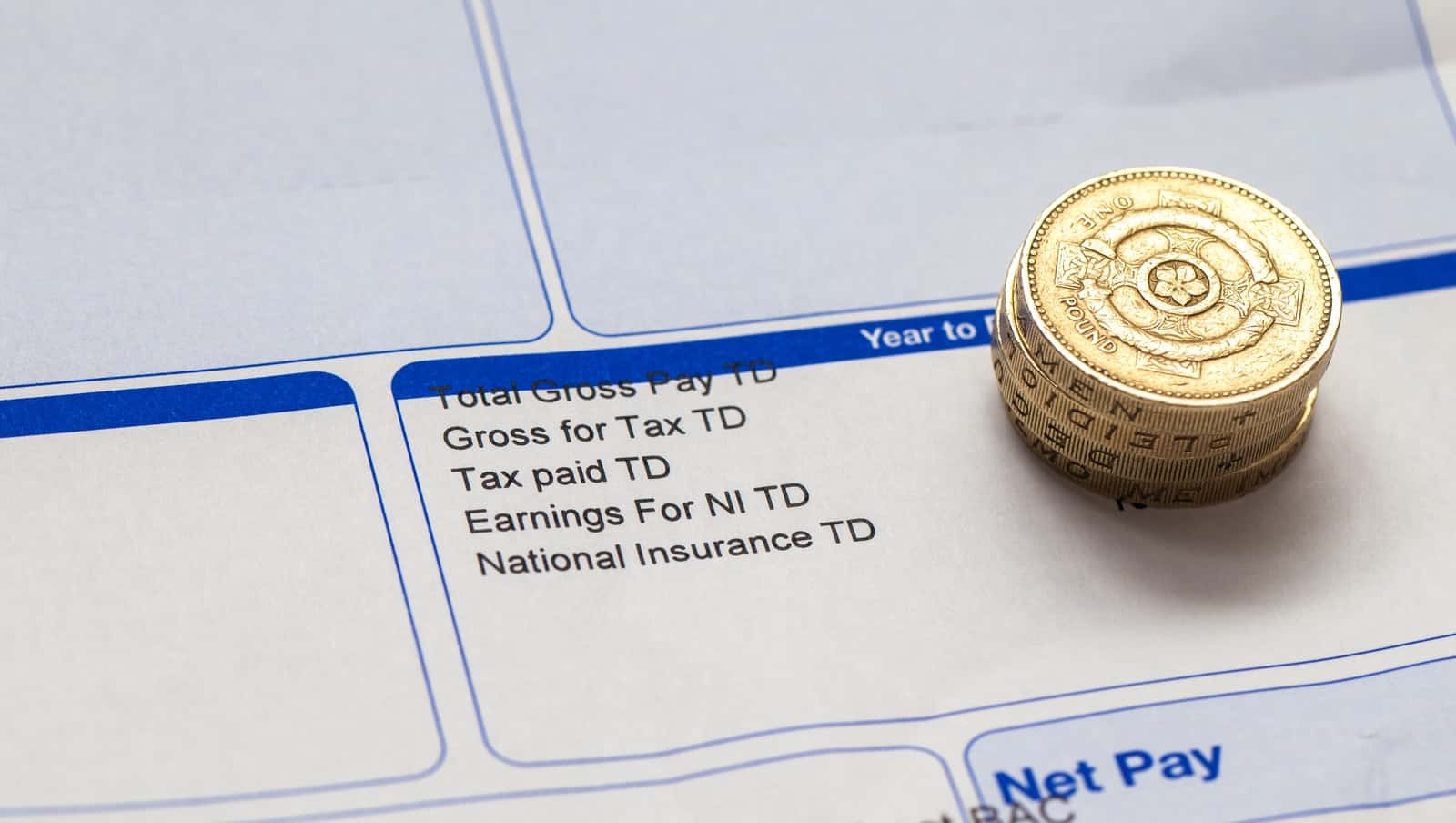

While your payslips don’t come from HMRC and so aren’t a PAYE tax form, they’re crucial to making sure you’re paying the right amounts for your deductions and keeping track of what you’ve paid. Tax and National Insurance are the most important ones here. This is because you’re accountable – not your employer – if you don’t pay enough. If you have a company pension or employer benefits that you pay for, these should show on your payslip, too. You’ll also be able to see a running total of the deductions you’ve paid for the tax year so far.

You should check that the payments for all deductions are as you expect. Make sure the deductions going out are correct, and any benefits you cancel stop coming out of your pay when you stop receiving the service. Discovering you’ve been underpaying for a benefit can come as quite a nasty shock when you have to catch up all of a sudden!

A P60

A P60 tax form is an “end of year” certificate that HMRC issue to everybody who has paid tax at the end of that tax year. Remember, the tax year runs from 6th April one year until 5th April the next. It’s normal to receive your P60 in April, May, or even in early June. In most cases, HMRC will send yours to your employer, who will then pass it on. Your P60 is vital proof that you’ve paid tax, which you may need to provide to claim back overpaid tax, or to apply for tax credits. You’ll also need your P60 as proof of your income when you apply for some loans or mortgages. So, it’s important that you read it carefully, and keep it filed safely.

If you have more than one job, you’ll receive a separate P60 from each of your employers. Your P60 details the total amount you’ve earned in that employment, and what has been deducted from your salary. This will include deductions for National Insurance, income tax and student loans if you pay it. Your P60 will also list your tax code as it was at the end of the tax year. It’s important that you check that all of the information on your P60 is correct, to make sure you’ve paid the right amounts in deductions.

Your P60, however, won’t cover deductions that have been taken automatically from your salary to contribute to your pension or pay for other benefits you receive from your employer. To check those, you should receive a P11D or statements from each benefit provider.

Read more: What does my tax and National Insurance pay for?

A P11D

A P11D is the HMRC tax form that covers the cost of benefits you’ve received through your employer, and the tax that’s due on them. Where you receive benefits that are taxable, and your earnings are above the £8500 threshold, your employer will calculate and automatically take the tax you owe through PAYE. How much tax you pay for your benefits depends on what they are, and what they’re worth. Some of the benefits you may pay tax on are:

- Company car

- Living accommodation

- Private medical or dental insurance

- Loans, such as for a season ticket, if they’re worth more than £10,000

- Subscriptions or memberships to professional organisations

Not all benefits are taxable, though. Benefits such as childcare, and meals you get for free from a work canteen, for example, are exempt from tax. Your employer should make it clear to you which benefits on offer are taxable, and which aren’t. If in doubt, though, check with your line manager or HR team.

Your P11D explained

When you receive a P11D, it will detail each of the different categories of taxable benefits. Where you’ve received a benefit, it will show the total cost to you, the amount your employer has “made good” by paying for you, and the cash equivalent you’ve therefore paid. To work out how much tax you’re paying on your benefits, look at the “amount made good” boxes. These show the benefit you’ve received from your employer through them contributing on your behalf, and this is what you pay tax on. You’ll only see values in the boxes for the benefits you’ve received. So, for example, if you don’t have a company car or receive a car allowance, these boxes will be empty.

In most cases, the tax you owe on your benefits will be deducted from your personal allowance and collected through PAYE. This means your tax code will be adjusted. If you’re ever unsure that your tax code is correct, check with HMRC directly, or with your HR or payroll department.

A P45

A P45 is the HMRC tax form you receive when you leave your job. You’ll receive a P45 irrespective of the reason you’re leaving; it’s the law. In some cases, you may need to request your P45 from your employer.

Your P45 shows how much tax you’ve paid in that employment so far in the current tax year. The form is split into four parts – 1, 1A, 2 and 3. Your employer will send Part 1 to HMRC directly, and will give the other three parts to you. You should keep Part 1A for your records, and give Parts 2 and 3 to your new employer. It’s important that you give your new employer these parts of your P45. They use them to work out your tax code and make sure you pay the right amount of tax now you work for them.

What if I don’t have a P45?

If you don’t have a P45 for whatever reason by the time your new employer asks for it, then they will likely ask you to complete a “new starter checklist”. This new starter checklist will give them the information they’d otherwise get from your P45 to calculate your tax code. This is why it’s so important that you receive and check your payslips, as you can use the running totals from your last payslip from your previous employer to fill this in accurately.

If you’re unable to provide information about your deductions from previous employment, then your employer may put you on an emergency tax code. This means that until you can provide them with the numbers and they can recalculate, you may pay more tax than you should. If this happens you will get it back eventually, so it’s not the end of the world. But it’s always better to have that money in your pocket than the tax man’s!

The lesser known HMRC tax forms: The P800

The P800 tax form is a less frequently used HMRC tax form, and many people have never received one and have never heard of them. You’ll receive a P800 if HMRC think you’ve paid an incorrect amount of tax at the end of the tax year. This could be an overpayment, in which case you’ll be due a refund, or an underpayment explaining that you need to pay more. It can take a while after the end of the tax year to receive a P800 if you’re due one. Sometimes, you won’t receive it until the end of November.

HMRC don’t always send a P800 in these situations, though. In some situations, they will send you a “Simple Assessment” letter instead. But, both do the same job. You may receive a Simple Assessment letter if the tax you owe can’t be automatically taken from your income, or you owe more than £3000.

Common reasons to receive a P800 include if you left one job and started another, but were paid by both employers in the same month. Or, maybe you started receiving a pension while still working, or were in receipt of Employment Support or Jobseeker’s Allowance.

Your P800 explained

Your P800 will show the income that HMRC think you should have paid tax on in that tax year. It’s important that you check this matches your other records, like your P60. The P800 will also show how much you’re due to be refunded if you’ve overpaid, or what you owe if you’ve underpaid. It will also explain how you can claim your refund, or how the additional money will be collected from you. Quite often, it’s possible for HMRC to recoup what you owe from underpayments by increasing your PAYE deductions.

If you think the information contained in your P800 is incorrect, then you should contact HMRC straight away. You only have 60 days to raise a query with HMRC if you think their information is wrong, so it’s important not to sit on this.